Case Study: Brabecan Services Limited v Commissioner of Domestic Taxes (Tax Appeal E780 of 2025) [2026] KETAT 22 (KLR) (9 February 2026) (Judgment)

Background

BSL, a filling station operator, was appointed by KRA as a VAT withholding agent pursuant to Section 42A of the Tax Procedures Act (TPA). KRA assessed BSL for Ksh. 1,872,158.00 for failing to withhold and remit 2% VAT on purchases for January 2025. BSL objected to the assessment, but KRA confirmed it on 9th June 2025. Dissatisfied with KRA’s decision, BSL lodged an appeal at the Tax Appeals Tribunal.

Procedural Competence of the Appeal

The Tribunal examined whether the appeal was properly before it and found a fundamental procedural defect

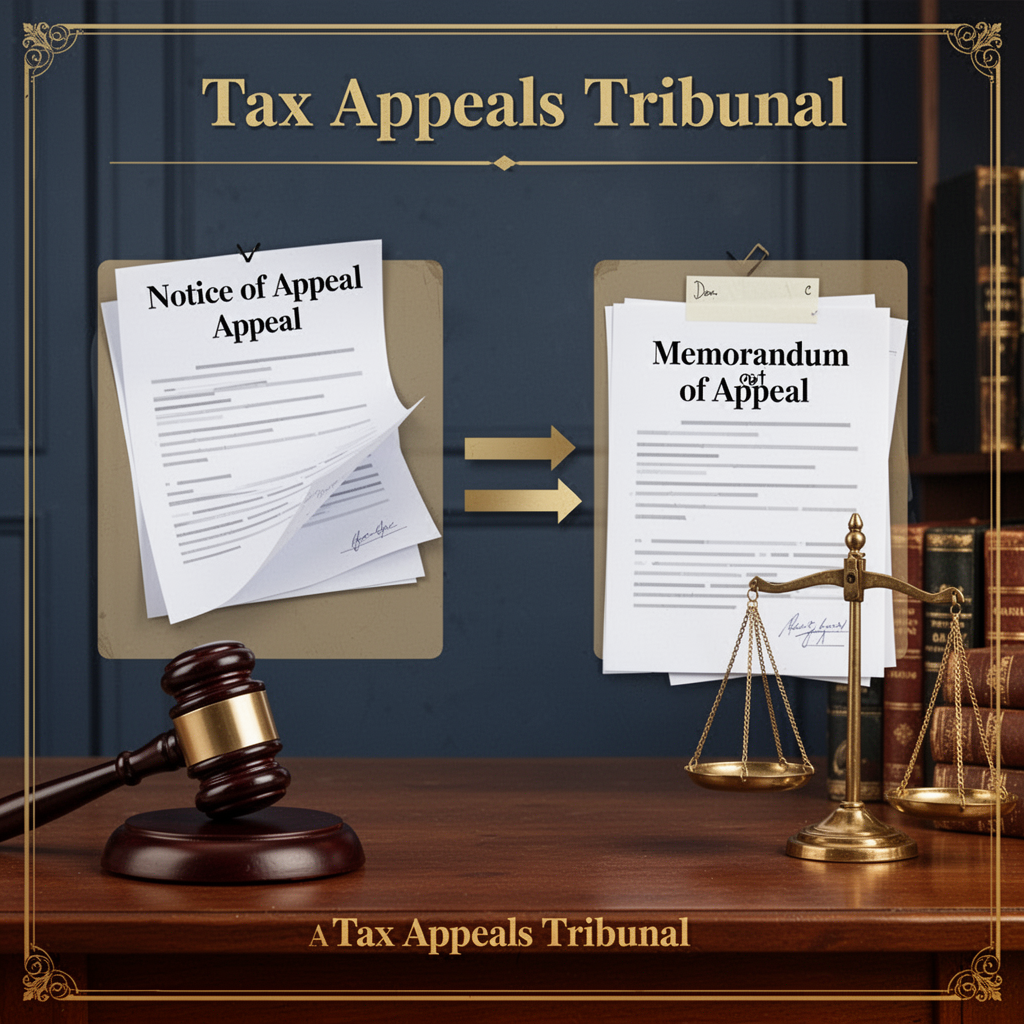

Statutory Requirement:

Section 13 of the Tax Appeals Tribunal Act (TATA) establishes a strict sequence:

- A Notice of Appeal must be filed within 30 days of the Commissioner’s decision.

- Second, within 14 days of filing that Notice, the Memorandum of Appeal, Statement of Facts, and other documents must be filed

Procedural Lapse by BSL:

- BSL filed its Memorandum of Appeal and Statement of Facts on 20th June 2025.

- BSL filed its Notice of Appeal later, on 15th July 2025.

- This reversed the statutory order. The core pleadings were filed before the document that invokes the Tribunal’s jurisdiction existed.

Legal Reasoning:

- The Tribunal held that the Notice of Appeal is the foundational document. Without it, there is no valid appeal, and any documents filed prior to it are not validly before the Tribunal.

- The subsequent filing of the Notice of Appeal on 15th July could not retroactively cure the irregularity, as BSL did not seek leave from the Tribunal to do so.

Final Decision

- The Appeal was struck out in its entirety for being incompetent.

- Each party was ordered to bear its own costs.

Key Takeaway

The case was decided purely on procedural grounds. Failure to follow the sequential filing requirements of Section 13 of the TATA (filing a Memorandum of Appeal before a Notice of Appeal) is a fatal jurisdictional error. The Tribunal did not consider the merits of the underlying tax dispute.